EAIS 2025 Wrap Up

Brussels, 31 October 2025

We are glad to announce that yet another very successful edition of the European Angel Investment Summit took place on the 28th and 29th of October 2025, gathering 300+ angel investors, entrepreneurs, policymakers, and thought leaders from across Europe and beyond!

This year’s summit tackled the key topics shaping Europe’s innovation landscape: from the 28th Regime and boosting private investment in European VC, to accelerating angel communities and enabling cross-border investing.

And because a change of scenery is always refreshing… this year’s venue made it even more special!

We were hosted at the European Commission Charlemagne building, a prestigious and highly exclusive headquarters at the heart of EU decision-making, rarely open to the public. An iconic setting that set the tone for high-level conversations and meaningful connections.

EAIS 2025 Key Takeaways:

As always, the Summit was a glimpse into the future of angel investing, and here you can read the main takeaways from the 2025 edition:

1. Speed matters.

New policies, financial instruments, and government processes must move faster to match Europe’s ambitions.

2. From plans to action.

Europe has the talent and resources — now it’s time to turn strategies into concrete results.

3. More angels, better incentives.

We need more angel investors and stronger incentives to keep supporting early-stage innovation that isn’t yet VC-ready.

4. Smarter co-investment models.

Governments can scale impact by creating accessible, long-term co-investment schemes with angels, both deal-by-deal and through SPVs.

5. Boost cross-border investing.

Tax benefits, public matching programs, and trust-building across countries are key to enabling more international deals.

6. Policy momentum.

Public entities are ready to rework outdated instruments and strengthen support for angel investors — the time to act is now.

And to top it off… we presented our brand-new EBAN Statistics Compendium 2024, our biggest annual publication packed with insights on Europe’s angel investing landscape! The compendium combines data from 35+ sources, including Dealroom.co, Crunchbase, PitchBook, and national VC associations, giving you a unique insight into Europe’s angel ecosystem.

Curious? https://www.eban.org/eban-annual-statistics-compendium-for-2024/

Also, we handed copies of our European Angel Co-Investment Schemes Proposal to the attendees. You can find it here: https://www.eban.org/european-angel-co-investment-schemes-proposal/

Huge Thanks

A huge thank you to all the speakers who shared their expertise, to the pitching startups, and to the hundreds of attendees who brought such energy and curiosity to the event. We’re especially grateful to our partners who helped make this happen:

- Connect2Scale

- egg Accelerator | Eurobank

- Enterprise Europe Network

- EU-LAC Digital Accelerator

- Hessen Trade & Invest GmbH

- Hoperfy

And we don’t forget about our amazing co-organisers:

What is coming next for EBAN?

As the European Angel Investment Summit 2025 in Brussels draws to a close, our excitement surges for what lies ahead at the next EBAN Congress in 2026. Set to take place in Vilnius, Lithuania, in collaboration with Lithuanian Business Angels Network (LitBAN), the 2026 EBAN Congress promises to uphold the legacy of excellence, knowledge-sharing, and networking.

Set in Vilnius, one of Europe’s fastest-growing tech and startup capitals, this two-day congress will provide an unparalleled platform to connect, learn, and invest in groundbreaking ideas while experiencing the city’s vibrant culture and hospitality. Attendees will engage in inspiring keynotes, interactive panels, investor–startup matchmaking sessions, and exclusive networking opportunities, all focused on the future of early-stage investment, innovation trends, and cross-border collaboration.

Block your Calendar for 1-2 June and make plans to be a part of the 2026 EBAN Congress in Vilnius. Together, let’s continue to push the boundaries of angel investing, provide invaluable support to startups, and actively shape the future of the global startup ecosystem.

The below one-pager was presented and handed out as part of #EAIS25. It is an initial proposal and a conversation starter with the EU and EIB group on creating an EU wide angel scheme that makes a huge impact on our market. Have a look:

EAIS One pager Co-investment Framework by EBAN

by Laurits Bach Sørensen, senior partner and co-founder at Nordic Alpha Partners, Europe’s leading greentech growth fund, & Jesper Jarlbæk, President of the European Business Angel Network (EBAN)

Europe stands at a decisive point in its industrial and energy transformation. The continent continues to produce world-class innovations in materials, energy, automation, and circular technologies, however far too few of these hardtech breakthroughs ever scale into globally competitive industrial champions.

Deeptech is entirely different from software and pharmaceuticals, and the companies in the hardware technology space need to be diligently scaled if they are to survive the valleys of death. The founder teams typically consist of a team of brilliant engineers, who need various operational guidance and a wide variety of support functions and capabilities to transform an idea into a profitable company.

One of the most pressing challenges is that the European venture capital model is less effective when it comes to managing the complexity and capex intensity of transformative hardtech, or deal with disruptive hypertransformation. The problem is not a lack of new inventions; it is a lack of operational capabilities and realisation that hardware-based transformative assets will not survive premature scaling on their route to market commercialisation.

Our proposal: Give experienced business angels a structural platform with access to the financial firepower and support capacities of European VC and PE.

If business angels were invited into or had access to more structured platforms and could use the same structures and financial engineering capacities that are usually reserved for growth equity firms, they could have a profound impact on the harder to grow technologies that fall outside the normal VC-model scope.

In fact, by combining the reach, structure and investment power of growth equity with the agility, network, and operational experience of business angels, we can target the critical growth phase (when advanced technologies transition from technological stability to product-market fit and early commercial scaling) and create immense value.

The traditional business angel in Europe

Typically, business angels have one of two backgrounds; type one is a successful entrepreneur that has taken a good idea and translated it into a commercially viable business, which has been exited to a strategic or financial acquirer (or sometimes via an IPO). The second type is successful business executives with comprehensive knowledge of best practices in leading multinational corporations.

In both instances, the business angels have relevant, first-hand operational experience, and a capacity as well as an appetite to engage in early-stage start-ups that appear to be higher risk. Business angels often form consortiums (to spread the risk) and provide the start-up with a lead angel that can channel all the relevant industry and necessary market knowledge from the angel consortium.

Building a company or developing a technology from a very early stage always involves timely identification of the barriers to growth and addressing them before the start-up hits a glass ceiling. As companies scale, several business functions evolve from being just a portion of some individual’s job description, to being fully fledged departments led by professional managers. Business angels have been through this development before and knows how to manage both cultural and organizational transformations.

Finally, the classic business angel understands the importance of diligent cash management and securing a profitable and de-risked offering. They also understand that premature scaling, especially when dealing with capex intense assets, is the fastest route to the valley of death. Also, when they engage operationally, the business angel won’t perceive the investment through a lens of: “1 out of X”. Instead, they are substantially more committed to the success and return of their direct investment activities.

Traditional VCs in Europe

The rationale of venture capital has been to take calculated risks on new and promising technology. They’ve traditionally done this by raising many but relatively small funds, typically from 25-100 million EUR. The funds then deploy the capital across a large spread of different, early-stage companies with the best roadmap and potential market fit.

The business model has been predicated on the fact that it can mitigate risk through diversity, with many VC investors utilizing a ten to one or even twenty to one approach, meaning that for every ten or twenty equity investments, one will drive sufficient returns to make up for the others, with money left over.

This model has worked well since it was professionalised in the 1970s and continues to work well within several different sectors, such as software and pharma, two areas where Europe continues to successfully commercialise a high number of new innovations.

How the current VC model is putting EU at risk of falling behind

With its many facets and completely new geopolitical reality, the classic VC model struggles to drive commercialisation of the next generation of technology assets in Europe, and this has created two major problems for our region:

1) The EU’s commercialisation rate is lower than other countries:

According to the EIB, VC investments in the US are 6–8x higher than in the EU. In the European Commission’s own Competitiveness Report from 2024 it stated that cleantech innovation in the EU “does not translate into a production advantage.”

In fact, the EU accounts for only 5% of global venture capital raised, compared to ~52% in the US and ~40% in China, a powerful indicator of the weaker commercialisation rate.

2) Industrialisation technology and “first-of-a-kind”(FOAK) industrial technologies are underfunded:

A fragmented EU capital market and the small size of the majority of VC funds in Europe do not provide the necessary scale-up capital for capital-intensive technologies. This was documented by the Delors Centre in 2024 in a report that confirmed that EU’s VC sector is smaller, with fewer funds, and that institutional investors rarely allocate to VC, creating a structural mismatch for industrial tech scale-ups.

New industrial technologies in particular require a blended capital stack (equity + debt/quasi-equity + grants), not pure VC. This issue has previously been raised directly by the EIB cleantech team. What happens is that FOAK (First of a Kind) technologies fall into a “no man’s land” as they are often too large for VC and too risky for traditional project finance. Lastly, it has been highlighted several times that European VC has a strong bias towards software, and InvestEurope estimates that “information and communication technology” received ~46% of venture investment, with biotech & healthcare receiving 27%.

But Europe and its member states won’t be able to defend itself from geopolitical warfare (as we have recently seen with China using access to lithium and rare earths as political mechanism) nor can Europe sustain growth on new software or obesity drugs alone. As a region, we need optimised heavy industries that can sustain themselves, an independent and efficient energy production capacity and a defense industry that can source and scale innovations locally.

Naturally, this requires that the financial ecosystem finds a way of investing into asset-heavy hardware technologies (You can find more information on what factors hardware companies have to navigate in this article on Hypertransformation).

How they have changed the VC model in China

China, one of the fastest growing economies in the world, have seemingly solved the issue of deploying the right amount of capital at the right time and in the right format, and according to Stanford’s Center on China’s Economy and Institutions they have done it through re-thinking and establishing thousands of government-backed niche VC funds.

These funds are dispersed across industries and regions, targeting critical technology niches. At the same time, these funds are deeply integrated into existing corporate environments, and with full overview of upcoming policy and regulatory changes, due to the long-term public planning structure. From 2013 to 2018, the number of government-backed VC funds surged, with an average of 238 funds created annually. Government-sponsored funds now account for +30% of all private equity and venture capital funds raised in China and together they can allocate almost 1 trillion USD to innovation within critical industries and technologies.

At the same time, the Chinese central bank recently extended its offering of a favourable interest rate for all initiatives with a “green” profile, currently at around 1.75% vs. the normal, nominal interest rate of around +4%. The country’s long-term strategy also enables it to implement policies that can quickly cater to new value chains and industries. As a result, China and Chinese firms now lead in 57 out of 64 critical technologies globally. In 2007, China led in just three of 64 technologies, according to the Australian Strategic Policy Institute.

Now, the European VC model cannot adjust to a similar degree, and neither should it, but it cements the argument from earlier, that we need to foster a new and deeper relationship between those with operational capabilities and those with capital.

A low, early-stage commercialisation ratio paralyses the critical interconnectivity in the financial ecosystem

Currently, the low success ratio of ensuring a profitable commercialisation of Europe’s strong industrial innovation, means that the later stage and much larger capital deployment players and growth supporters cannot get involved. They simply have very different requirements in terms of risk/revenue/profit & loss, and also very different investment horizons and return commitments.

The conventional growth equity and buyout investors are simply not able to take the risk nor spend the time to lift new technologies up to a state of profitable industrial grade performance. In effect, this means that despite interest and capacity to invest in the scale up phase, they will not engage as the private equity model is not tuned to drive return unless the companies they invest into have reached a sufficient level of financial maturity.

The unfortunate effect of this “gap of engagement” in the financial eco-system is clearly visible in the declining number of IPOs. It also has a critical effect on large scale infrastructure capital players, when technologies don’t reach critical mass. In essence, they either are or will be starved of new assets to invest into.

On the sidelines of an interconnected financial ecosystem in Europe, we have the 15 trillion USD capacity of the European pension funds. They however struggle to see the argument for making returns in a financial value chain with such a strong disconnect between innovation and large, established industrial players.

Ultimately, all of this negatively affects Europe’s ability to convert its strong innovation into GDP growth, as new companies that can contribute to overall growth are not reaching sufficient scale.

Recent examples of larger projects with huge commercialisation difficulties include:

- Northvolt (Sweden, industrial/cleantech): Europe’s flagship battery start-up raised 15 billion EUR through heavy reliance on state guarantees, EU and pension fund-backed financing (ATP, EIB, EIFO, etc.), and corporate anchor customers like Volkswagen. However commercialisation and reaching industrial grade production proved more difficult than anticipated, leaving it to get bought out of bankruptcy proceedings for just 200 million USD by a US-based startup.

- Stegra / H2 Green Steel (Sweden, industrial/cleantech): Europe’s big bet in terms of creating a green-steel plant launched with 6.5 billion EUR in planned financing, backed by EU and state support, pension funds, and corporate offtakers such as Mercedes-Benz and Scania. Its Boden, Sweden plant was designed to deliver 2.5 million tonnes of near-zero carbon steel annually by 2030, powered by green hydrogen and renewable electricity. However, escalating costs, delays, and a shortfall in expected state aid have forced the company to seek another 975 million EUR in emergency funding, while media reports suggest it faces acute financial distress and potential insolvency.

- Skeleton Technologies (Estonia, ultracapacitors): A deeptech hardware player with strong potential in energy storage. It has raised significant VC funding but repeatedly flagged that European growth financing is shallow compared to the US or China, slowing down industrial rollout.

- Nilar (Sweden, batteries): Developed innovative nickel-metal hydride storage systems but has struggled to secure the scale-up capital needed to compete internationally, underlining Europe’s gap in patient industrial capital.

Solar manufacturing (Germany, Spain, Italy): Europe once had a thriving solar PV industry (Q-Cells, SolarWorld, Solaria). Most collapsed or were acquired after Chinese firms, backed by coordinated state policy and patient capital, scaled faster. Today, Europe imports the vast majority of its solar hardware, despite being an early innovator.

Thinking beyond Technology Readiness Levels and revenue

One part of the equation around the lack of commercialisation is that many early-stage players think that it is enough for a technology to be functional for it to convert a market.

Only later do they realise that technologies that are seemingly great on paper and are at TRL 9 level, are very far from being industrial grade.

Northvolt is a good example of a TRL9 technology that came shooting out of the gates with both VC and industrial backing, but without any existing value chain or supporting ecosystem, referred to as TRL10. And many early-stage investors also underestimate the importance of ensuring capital efficiency and functioning value chains in their scaling strategy and instead overly focus on creating or generating revenue, regardless of cost.

However, when dealing with industrial technology in fast-growing sectors with high demands for new offerings, locking your company into contracts that forces you to suddenly build stock and deliver hundreds or thousands of units or solutions without sufficient margin, more revenue can become far more dangerous than less revenue. We refer to this as “premature scaling”.

Political stability also plays a role in the TRL10/industrial value chain discussions, something that China has solved for in a very efficient way, as mentioned, through long-term roadmaps and accelerated market demand into a much less fragmented market with more transparent legislation. This enables them to fund assets for longer, deploy more operational support functions and secure industrial grade quality/readiness before considering an exit.

As said, we can’t replicate that model in Europe, but what we can do is give the thousands of expert business angels access to new tools and more powerful structures such as new vehicles and dedicated financing.

Equipping business angels with the firepower of private equity

While business angels are skilled in the operational reality on the asset level and the complexity of scaling a founder-led business, they are often small “one-person” entities without vast access to financial engineering infrastructures, value creation support services, specialist technology advisors or the many support functions that are core to the private equity and venture capital toolkit.

This is also the reason why we won’t fix the problems just by putting more money into the hands of the business angels. Instead, we need a more structured approach to upskilling business angels, bringing them closer to the growth equity community or create a vehicle that resembles the VC/PE format but with more operational knowhow.

If we can create a stronger platform for cross-collaboration between these two early-stage players, with new models that can deal with the complexities of hypertransformation – then we can increase the capital efficiency across the growth cycle and ultimately end up with more quality technology assets, for the conventional growth and private equity investors to scale up, in a shorter amount of time.

A new form of such collaboration between growth equity (VC, PE, INFRA) and experienced and operationally engaged business angels armed with an operational value-creation toolkit tailored to scaling industrial technology could be in the shape of a new and integrated early-stage investment entity.

A vehicle that could merge the reach, structure and financial firepower of professional growth equity, with the agility and operational experience of business angels. By equipping business angels with professional tools, shared value creation services, talent infrastructure, and co-investment capital, they could facilitate a more de-risked and faster journey from early stage to industrial maturity. In essence, such a structure would provide business angels with the power of private equity: full access to vetted deal flow, value-creation services, venture capital levels of syndication capital, and multiple exit or liquidity routes – from early secondaries to full-scale international expansion.

Some core elements that would differentiate such a vehicle from both traditional business angel syndicates and conventional venture capital models include:

- Addressing the hard-tech scale-up challenge by mastering hypertransformation.

Industrial and hardware-based technologies rarely fail because of the product – they fail because of the overwhelming complexity that emerges when trying to scale technology, operations and capital in uncertain regulatory regimes across multiple geographies and value chains. This phase demands a level of governance, speed, and integration that most early-stage companies – and their investors – are unprepared for. There are several ways to teach skills necessary to navigate this. One is by building and incorporating bespoke executive programmes. One such programme that NAP has already built is the “Global Re-Industrialisation Programme” in partnership with the Danish Technical University (DTU). - Giving access to systematic value creation powered by proven toolkits.

Nordic Alpha Partners has already prepared to release its full value creation and management toolkit in book form. Covering the creation, de-risking and management of hypergrowth at the earliest stages while bringing institutional-grade structure, strategy, and data discipline to young industrial technology companies. - Offering flexible and secure liquidity models, meaning predictable return pathways for investors.

Such a platform could introduce a new level of liquidity visibility and structural flexibility to the business angels as it would set up structural partnerships with conventional VC and growth funds. Funds that are looking for de-risked assets and are eager to buy secondaries to secure them. At the same time, each company’s journey would be fully mapped from the outset, defining the expected strategic trajectory and the liquidity (exit) options available at key milestones. This ensures investors are never locked into a binary exit scenario but instead benefit from multiple, pre-engineered outcomes—including full exits to later-stage investors, partial exits to realise early returns, or continued ownership and co-investment alongside a growth fund. By combining disciplined planning with optionality, a platform like this could provide a predictable, de-risked liquidity profile. Something that is very uncommon in early-stage investing otherwise, allowing angels to balance short-term return potential with long-term value participation.

Overall, there are numerous ways for new structures to support early-stage industrial investing, but merging the strengths of entrepreneurial agility, institutional structure, and financial professionalism is in our view a unique combination to better activate the full financial ecosystem.

Providing investors with exposure to a de-risked, systematically managed early-stage portfolios, and leveraging Europe’s strong angel community, strong VC community, and the other parts of the financial ecosystem, we could vastly improve the success rate of European greentech and industrial innovators.

An obvious partner for such a concept is the upcoming “European Scale-Up Fund”, a partnership between the EIF and the private investment community. It creates a strong player in the ecosystem that can provide great support avenues for founders and promising technologies along the way.

However, without a pipeline of high quality and de-risked assets, there is a risk that a fund like the Scale-Up Fund will have to lean into Venture Capital risk rather than scaleup growth equity.

Business angels are they key to activating the broader ecosystem and increase the quality and commercialisation of early-stage technology.

Summing up:

- Europe is facing a new normal and the current early-stage investment model is evidently ill-equipped to boost European resilience technologies and competitiveness overall.

- We need to rethink Europe’s early-stage model if we want to keep up with the US and China, as well as new and emerging economies such as India.

- Right now, Europe’s “army” of business angels needs to be utilized much better. They are the key to unlocking Europe’s commercialisation potential.

- All the components are available to us, and if we are able to set it up in large enough scale, we can enable the rest of the financial ecosystem to enter into the hardware sector and support the emergence of critical new industrial technologies. This way, we can ultimately boost GDP growth and secure stronger returns to Europe’s pensions funds, and increase resilience across the market.

About EBAN Europe

The European Business Angel Network (EBAN) is Europe’s largest trade body for angel investing, founded in 1999 and based in Brussels. The EBAN community includes over 10,000 individual angel investors and more than 45000 investors across multiple networks and sub associations.

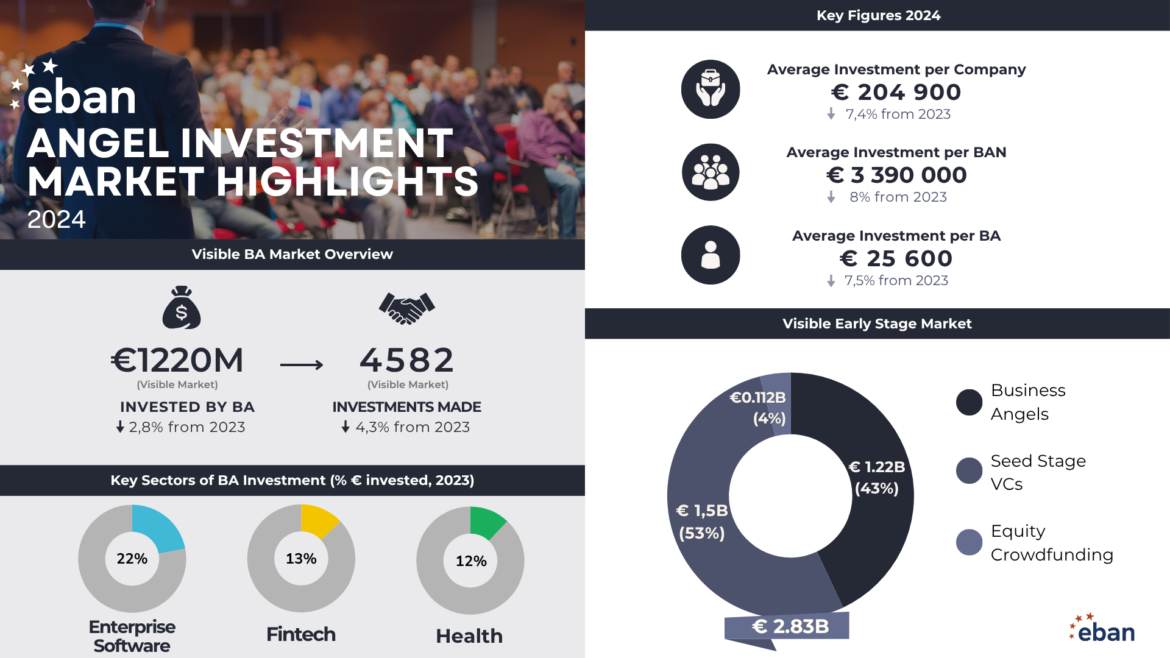

The network spans more than 50 countries, and figures from 2023 puts capital deployed at around EUR 1.2 billion across 4,789 angel-involved funding rounds.

In 2023, the three largest countries in terms of angel investment commitments were the UK (EUR 307.4m), Germany (EUR 198.5m) and France (EUR 142.5m).

EBAN estimates that angel investments account for roughly 50% of European early-stage investments in 2023, with the rest stemming from direct VC (40%) and a small proportion coming from equity crowdfunding (friends, family and fanatics) (10%).

In recent years, there has been strong growth of angel investment in energy sector startups across both 2022 and 2023, which now account for 10% of total investments in the early-stage investment ecosystem, with deeptech accounting for 6%

About Nordic Alpha Partners

Founded in 2017 and now with ~400mEUR in assets under management, Nordic Alpha Partners is a European resilience and green technology fund with a unique model, deeply focused on active ownership and operational value creation.

The fund works in close cooperation with the business angel community in what the fund calls a nesting fund structure, where business angels are provided with deal flow that contains asset opportunities that are too early for NAP to invest in. When BA’s mature them to a state of de-risked commercialisation, then the NAP flagship fund can invest and lead the globalisation.

In general, NAP is deeply engaged in creating an interconnected and coherent financial value chain for resilience and complex industrial technologies in Europe. We do this via deep cooperation with both the academic and innovation environment, doing research and established bespoke educational programmes like DTU GRIP, the BA community via its nesting fund activities, partnerships with more than 50 VC funds as well as large scale green industrial infrastructure capital players (Copenhagen Infrastructure Partners owns part of the NAP management company).

The firm was built on the thesis that a new and operational value creation toolkit could support complex deeptech and industrial decarbonisation technology companies through the challenging scaling phase. The result has been above-normal return opportunities in sectors where conventional private equity models are ineffective.

To date, the firm has raised over 1bn EUR directly and indirectly for companies at the forefront of the green transition.

With CAGR of 65% and annual related and equivalent emissions reductions across the portfolio in excess of 850.000 tons CO2e, the model continues to drive growth and value in areas otherwise avoided by private equity.

To do this, more than 50% of all team capacities and 60% of the partner group are fully dedicated to operational value creation through the deployment of the fund’s own value creation toolkit.

The Nordic Alpha “playbook” is being published in early 2026, so that the financial ecosystem can adopt or take the most useful methods from NAP’s systematic approach and decades of experience on how to diligently scale complex industrial technology. The assumption is that uniform language and methods can enable large scale activation of the market capital and illustrate how hardtech and industrial investments can deliver above normal returns.

For further insights on complexity of “Hypertransformation” and the challenges in Europe, please see the following publications: European Business Review 1, European Business Review 2, EnergyWatch, NewWave Podcast.

October has been an important month for the CLARIFAI project as it has taken key steps toward shaping the future of impact investing through artificial intelligence. The team had the opportunity to present the project at two major events: the Kick-Off Meeting in Brussels, organised by the European Commission, and The Gap in Between, held in Valencia.

The Gap in Between in Valencia on October 21st

The CLARIFAI team joined The Gap in Between, held at La Marina de Valencia. The panel “The Future of Impact: Insights from Leaders in Investment and Innovation” convened leading investors, founders, and ecosystem pioneers to discuss how intentionality, data, and technology are transforming impact investment.

Featuring Christina Figiel (BetterVentures), Juan Fuentes (EBAN), Tom Novotny (Impact Angel), Johan Morales (Zubi), and Venkata Gandikota (InnoFrugal AI for Impact), explored the nuances of aligning financial sustainability with genuine social and environmental outcomes. Speakers emphasised that intentionality and impact must be embedded within the business model, coexisting with financial validity. They noted that not every investor fits every founder, especially in impact investing, where greenwashing risks remain.

The discussion highlighted the importance of proxy metrics, education, employment outcomes, and gender and diversity considerations, including board composition, as key impact levers. The panel also underscored the role of communication and the limitations of single KPIs, while exploring the potential of AI-driven assessment.

During the session, Tom Novotny introduced TAU20, an AI-powered platform designed to make impact assessment more transparent, efficient, and actionable for both startups and investors. Closing remarks highlighted TAU20’s role as a next-generation impact intelligence tool and invited participants to collaborate in shaping the future of responsible, data-driven investment.

Introducing CLARIFAI to the European Innovation Community in Brussels on October 22nd

Shortly after Valencia, the CLARIFAI team participated in the Kick-Off Meeting for projects funded under the ESF-2024-SOC-IMP – Actions to Develop Impact Performance Intelligence Services for the Social Impact Investing Market Actors. The event took place at the Youth Hostel Jacques Brel in Brussels and was organised by the European Commission’s DG Employment, Social Affairs and Inclusion (DG EMPL).

Besides networking with sister projects, one of the most engaging moments was the pitch session, where the team presented TAU20 to the jury panel. Projects were distributed between two panels; the session featured Liz Fleming (Chief Ecosystem Officer, South Summit), Cyril Gouiffes (Head of Social Impact – Equity Investments, EIF), Rob Symes (CEO, Fortell), and Claus von Riegen (former Head of Strategy, New Ventures & Technologies, SAP). The team was also able to engage with Giulio Pasi (Call Coordinator), Axel Specker (Project Officer), and Brigitte Fellahi (Head of Unit, DG EMPL).

About CLARIFAI

The CLARIFAI project is developing an AI-powered SaaS platform to enhance decision-making in the impact investment market, particularly for early-stage startups often overlooked by traditional ESG metrics. Through comprehensive market research, stakeholder engagement, and real-world testing, the platform is being designed, prototyped, and refined based on user feedback, with a scalable business model and go-to-market strategy in place. By analysing qualitative impact data with AI, CLARIFAI aims to improve transparency, standardisation, and efficiency in impact investing, helping investors and startups make smarter, faster decisions while reducing impact-washing. As adoption grows, the platform will align with global standards, foster market trust, and drive data-driven innovation, ultimately transforming the sector with scalable tools that enable sustainable, long-term social and economic impact.

About EBAN

EBAN – European Business Angel Network – is the European association for business angels and other early stage investors. Our mission is to drive successful and responsible early stage investing by providing our members network connections, best practices and representation towards governmental stakeholders. Our association is a network of networks that gathers thousands of professional investors across Europe and the rest of the world.

Around the world, countries are racing to harness the potential of Artificial Intelligence (AI). Today, the European Commission set out two strategies to ensure Europe stays ahead, driving adoption in key industries and putting Europe at the forefront of AI-driven science. The Apply AI Strategy sets out how to speed up the use of AI in Europe’s key industries and the public sector. The AI in Science Strategy focuses on putting Europe at the forefront of AI-driven research and scientific excellence.

Pension funds are the cornerstone of long-term investment in Europe. With their ability to deploy patient capital, they are uniquely positioned to fuel innovation, accelerate the green and digital transition, and strengthen Europe’s economic resilience. Venture capital, in turn, is the asset class that drives breakthrough technologies and high-growth companies.

Yet, while US pension funds allocate over 10% of assets to private assets, European pension funds invest less than 0.1%. This report explores the reasons behind that gap, the structural barriers holding Europe back, and the opportunities to unlock pension capital for innovation, growth, and competitiveness.

Europe’s Opportunity

Europe’s innovation economy faces a capital paradox. Despite global leadership in science and technology, European startups often lack access to the long-term capital needed to scale. Pension systems still rely heavily on pay-as-you-go models, leaving few investable assets.

The Draghi Report on European competitiveness made it clear: without stronger participation from institutional investors, Europe risks losing ground in the global race for innovation. The data confirms it, while European startups can raise significant early rounds, far fewer reach unicorn scale compared to their US peers. The gap widens as funding amounts increase.

The egg, the business accelerator of Eurobank, is returning for another year at the European Angel Investment Summit (EAIS25), taking place on October 28–29 in Brussels, bringing three fresh startups and empowering them to scale internationally. The egg’s participation in EAIS once again reflects the strong partnership and cross-border collaboration with EBAN.

The European Angel Investment Summit is the leading platform for dialogue between EU institutions and the world of angels, VCs, and startups to shape a stronger innovation ecosystem together. Organised by EBAN in partnership with the InvestEU Portal and the European Commission, EAIS25 is where the startup and investment community unites to voice its needs, share practical solutions, and form policies that make Europe the best place to start, scale, and invest in impactful ventures.

This year, the egg is showcasing three high-potential startups chosen for their innovation and scalability. Each will participate in a sector-specific pitching session:

- Timing for Sports: An advanced platform optimising athletic performance and training through data-driven insights.

- MOVE ON: A tech-driven solution transforming urban mobility and sustainable transport.

- Bitrezus: Dual-use cybersecurity platform designed specifically for satellite systems (space segment, ground segment, and communication links) and critical infrastructure.

For more information about EAIS25 and to view the full agenda, visit: https://www.europeanangelsummit.com/programme

About EBAN

EBAN – European Business Angel Network – is the European association for business angels and other early stage investors. Our mission is to drive successful and responsible early stage investing by providing our members network connections, best practices and representation towards governmental stakeholders. Our association is a network of networks that gathers thousands of professional investors across Europe and the rest of the world.

About egg

Established by Eurobank, egg is one of Greece’s leading Business accelerators, supporting startups grow through mentoring, training, and access to networks and funding.

As angel investing becomes increasingly professionalised across Europe, a compelling trend is emerging; generalist approaches are giving way to sector-specific strategies. “Invest in what you know”, a common advise by some of the most experienced and successful business angels. Angel investors are narrowing their focus, aligning with sectors where they contribute not only capital, but also deep expertise, networks, and credibility. This shift reduces risk and enhances value creation—benefiting both investors and start-ups.

Smart Capital in a Fragmented Landscape

In today’s fragmented start-up ecosystem, competitive advantage lies in smart capital—being able to identify and support the right team, in the right space, at the right time, with the right kind of backing. However, this evolution also brings challenges.

National Deal Flow Isn’t Enough

Sector-specific investors often face a paradox: their national market may not generate sufficient deal flow to match their investment thesis. For instance, an angel focused on sport or space may find that quality opportunities in their country are either too few, too early, or too late.

The solution? Go cross-border. But that’s easier said than done.

The Complexity of Cross-Border Angel Investing

Cross-border investing today comes with a host of complications: legal, tax, regulatory, cultural, and operational. Unlike venture capital firms, which have teams and advisors to support international deployment, market analysis, and cross-border networks, individual angels often lack the resources to navigate these complexities alone. This creates a gap in the ecosystem—one that EBAN communities are uniquely positioned to fill.

EBAN Communities: Reducing Friction, Increasing Impact

EBAN communities create structured, trust-based environments that connect angels across Europe and beyond. They help reduce friction in cross-border investing by offering:

- Shared deal flow: Access to qualified start-ups aligned with sector-specific theses, regardless of geography

- Sector expertise & networking: Communities bring deep know-how and international contacts

- Local knowledge bridges: Members from each country help navigate legal, regulatory, and cultural nuances

- Cross-border co-investment: Frameworks and best practices for efficient syndication

- Thematic clustering: Communities organised by sector or impact theme, rather than geography

Recent examples include EBAN Sports and EBAN Space & Defence, which demonstrate the growing momentum behind this model.

The 28th Regime: Enabling the Next Phase

Europe is moving closer to a unified framework for cross-border investment, often referred to as the “28th regime”—a harmonised legal and tax infrastructure that will simplify transactions across member states.

For sector-specific angels, this regime is not merely a policy milestone—it’s a practical enabler. It will allow them to look beyond borders for the best start-ups and act on those opportunities with greater ease and confidence.

Together, the 28th regime and EBAN’s sector-driven, cross-border communities form the foundation for the next evolution of early-stage investing in Europe: smart, connected, and international from day one. This will empower start-ups to scale faster and more efficiently, backed by capital that brings strategic value and market access.

Not Just More Deals—Better Ones

Ultimately, the goal isn’t simply to do more deals—it’s to do better deals. Sector-specific communities, powered by trusted cross-border networks, enable investors to find start-ups that fit their thesis and add strategic value.

When angels act as more than just capital—serving as mentors, connectors, and champions—start-ups gain a competitive edge. In a global, highly competitive market, that edge can make all the difference.

As Co-Chair of EBAN Sports, I encourage BANs and all BAN members interested in sport to join the community, with the hope that it will bring value to the EBAN ecosystem and foster innovation and early-stage investment in Europe across sports tech start-ups.

About the author

Juan Fuentes (Spain) is the Director of the Global Sports Testing Lab stablished in Valencia by GSIC (Global Sports Innovation Center) Powered by Microsoft, a global sports innovation hub funded by the tech giant. Juan is also a cross-border angel investor & mentor in start-ups, with several years of expertise in international business development in Europe, Middle East & Asia. He is FIBAN member, advisory board member in the Factory Sports Tech VC (Norway) and board member in Danish Start-up Group.

With over 9 years of experience working as LALIGA head of expansion in MENA and Northern Europe, his expertise in the sports industry combines with an agnostic approach as he also worked in MENA for the Spanish Embassy helping Spanish companies to expand globally, and in APAC in economic research and investment analysis for Oxford Business Group. With angel investments in 6 countries, he was also a mentor in TechStars US accelerator. He is an instructor and researcher in his fields of expertise in different universities: Harvard Business School, Stockholm School of Economics or European Sports Business School among others.