Over two days in early June, the 2026 EBAN Congress in Vilnius brought Europe’s angel-investing community to Vilnius for the 26th edition of the Congress, co-organised by EBAN, LitBAN, and the European Commission.

I attended with TechAngels Romania, an EBAN-member network focused on tech startups, to sharpen my own investing and due diligence practice and to understand how other European angel communities are approaching early-stage investing.

The event ran across one main stage and two secondary stages and included panels, fireside chats, and startup pitches across a wide range of sectors: from university spin-offs and angel governance to space and defense infrastructure, CleanTech, BioTech, CreativeTech, and SportsTech.

What made the event useful was not only the range of topics. It was that the same practical question kept coming back from different angles:

How do you turn technical expertise into fundable, usable companies?

The answers included the right team and timing, clear founder roles, fast customer feedback, disciplined investor follow-up, and early choices that make later funding rounds easier.

Below is a selective recap based on sessions attended, pitch notes, and conversations around the event. My goal is to share the patterns that stood out across the event, and the practical takeaways that I found most useful.

From Technology to Investability

The investability question showed up early in the university spin-off and angel-investing sessions. Laura Anne Edwards set up the question well in her talk on moving from class to industry.

Her core point was simple, but important: strong technology is not automatically a business. A technology can be impressive, defensible, and full of potential, while still not being ready for a company, a CEO, a fundraising round, or a specific market window.

That same idea came later in the panel on the anatomy of a fundable spin-off.

"The Anatomy of a Fundable Spin-off", featuring Péter Kristóf (Óbuda University), Gražina Mykolaitytė-Nielsen (VUGENE/LithuaniaBIO), Franziska P. Bäurle (DEFCOM Holding), Isabel Antholz (xscalyn); moderated by Laura Anne Edwards (NASA Datanaut, Oxford Space Initiative)

The discussion was less about better pitches and more about the ingredients that make a research/tech-heavy company investable:

Founder role clarity: the inventor is not always the best CEO, and that should be treated as a company-design question rather than a personal failure.

Co-founder trust: finding someone who is complementary matters, but trust should be treated as the minimum requirement.

Learning speed: early progress also includes how fast a team can test, learn, and adjust.

Customer feedback: deeptech teams still need market contact in the early stages, even when the technology path is long.

Investor and cap table discipline: warm interest can cool quickly, and early equity mistakes can make later rounds harder.

The “Mistakes that made us wiser angels” panel later added the investor-side version of the same idea. It warned against falling in love with the technology, investing without enough domain understanding, underestimating governance and board-seat dynamics, or acting alone when a syndicate could help reduce blind spots

"Mistakes that made us wiser angels", featuring Michael O'Connor - CorkBIC, Rita Anson - Nordic Ignite Angel Fund, Tuomas Pahlman - Hophopo.io, Marcel Dridje - Sophia Business Angels; moderated by Lina Vaitiekūnienė - Widen

In a separate session, Mary McKenna, in conversation with Rita Sakus, brought things back to founder psychology: resilience, focus, coachability, and the ability to recover after rejection are all things that investors take into account.

"Angel Investment Success and Failure", featuring Mary McKenna MBE - AwakenAngels/Learning Pool, Rita Sakus - LitBAN

Different Risks for Different Sectors

The same theme became more visible in the sector-specific sessions and pitch batches spread throughout the two days.

These did not feel like generic startups with different sector labels. Each one was dealing with the realities of its own market: who buys, how procurement works, what data can be used, what regulation allows, what infrastructure is needed, and how much capital the company needs to survive.

Space, defense, and infrastructure

Space and defense were perhaps the clearest example. Across both sessions and the startup pitches, space kept showing up as a strong focus on infrastructure: access, manufacturing, data, sovereignty, Earth observation, radiation monitoring, and cooperation.

Matthias Spott used a “reverse pitch”-style talk to argue that Europe should not simply copy the leading playbook for competing in space launches.

"The Geo-Strategic Relevance of Space & Defence Investments", featuring Matthias Spott (SPRIN-D/LEOconomy)

Instead, it should look for places where it can leapfrog: low Earth orbit infrastructure, the lunar economy, microgravity production, sovereign access, and industrial use cases that make space useful beyond the familiar launch domain.

Tuva Cihangir Atasever added the scientific and industrial layer. Microgravity was presented as an environment where materials, biology, tissue research, plant physiology, radiation measurement, and manufacturing can behave differently.

"Science in Space", featuring Tuva Cihangir Atasever (astronaut at the Turkish Space Agency)

In a separate session, Adrian Flynn talked less about rockets or hardware, and more about the human side of space cooperation: the relationships, trust, and cross-border networks that make long-term collaboration possible.

"Building an Ecosystem: Bold Collaborations Across Disciplines", featuring Adrian Flynn (The Karman Project)

For investors, that matters because space companies often depend on public agencies, international partners, and credibility that cannot be built at the last minute.

The startup pitches across this domain showed how these ideas can become concrete companies.

Zero Gravity Thermal worked around high-resolution thermal Earth observation. Spheer focused on making Earth observation easier to use for organizations without specialist satellite-data teams. OCCAM Space addressed the less glamorous but mission-critical layer between launchers and payloads: deployment and separation systems.

Dr. Olga Bodet pitching Zero Gravity Thermal

These and others turned technical ambition into practical due diligence questions: who validates it, who buys it, what infrastructure does it depend on, and what kind of public-private collaboration is needed for it to scale?

BioTech, CleanTech, and proof before scale

BioTech and CleanTech asked a different version of the same question: what proof is needed before scale becomes credible?

In the BioTech and life-sciences pitches, it was not only whether the science sounded promising (it did). It was what evidence, validation, regulatory path, customer demand, and commercial focus would be needed before the company could scale.

Startups pitching included VUGENE, which pointed to a practical bottleneck: drug-development teams need better ways to interpret biological data. OWL Lifesciences focused on disease models that could help therapy teams work with better data before clinical trials, while LifeGlue Technologies presented biomaterials for companies building artificial human tissues.

Laura Kuittinen pitching LifeGlue Technologies

Startups featured reLi Energy, which helps large-scale battery operators understand and optimize the real-time cost of each charge and discharge decision. CYNiO showed a way to make specialty isocyanates, chemicals used in high-performance materials, using CO2, while astracite presented a battery-material approach based on CO2 and silicon, with a focus on European supply chains.

Laura Laringe pitching reLi Energy

For investors, the useful question was: what proof would make the next step more credible?

In BioTech, that might mean better data, customer use, regulatory progress, or a clearer product focus. For industrial and climate-related companies, customer proof can mean paid pilots, measurable operational improvement, integration into existing systems, and evidence that the economics are strong enough for a buyer to change behaviour.

CreativeTech, SportsTech, and distribution

The CreativeTech and SportsTech pitches showed another kind of sector specificity.

MusicGurus connected music learning to content creation, licensing, distribution, and monetization for musicians, and Artist Arena sat closer to the relationship between artists, collectors, and digital/physical ownership.

Tome Rogers pitching MusicGurus

In these cases, the investor angle was less about lab validation and more about how audience access, rights, creator economics, and repeatable distribution turn into business.

A later CreativeTech panel on IP, risk, and scale (with) raised a related point: European creative and cultural companies may need to own more of their own infrastructure, instead of relying entirely on large platforms for distribution, audience access, and monetization.

"How Investors Should Assess IP, Risk and Scale in Creative Tech", featuring Kadri Harma (games/tech investor), Fredrik Sologub (Artist Arena), Matti Rönkkö (Kiilto Ventures), Anette Schaefer and Javier Arias (EIT Culture & Creativity)

SportsTech had its own version of that problem, focusing on how engagement can become a durable business model.

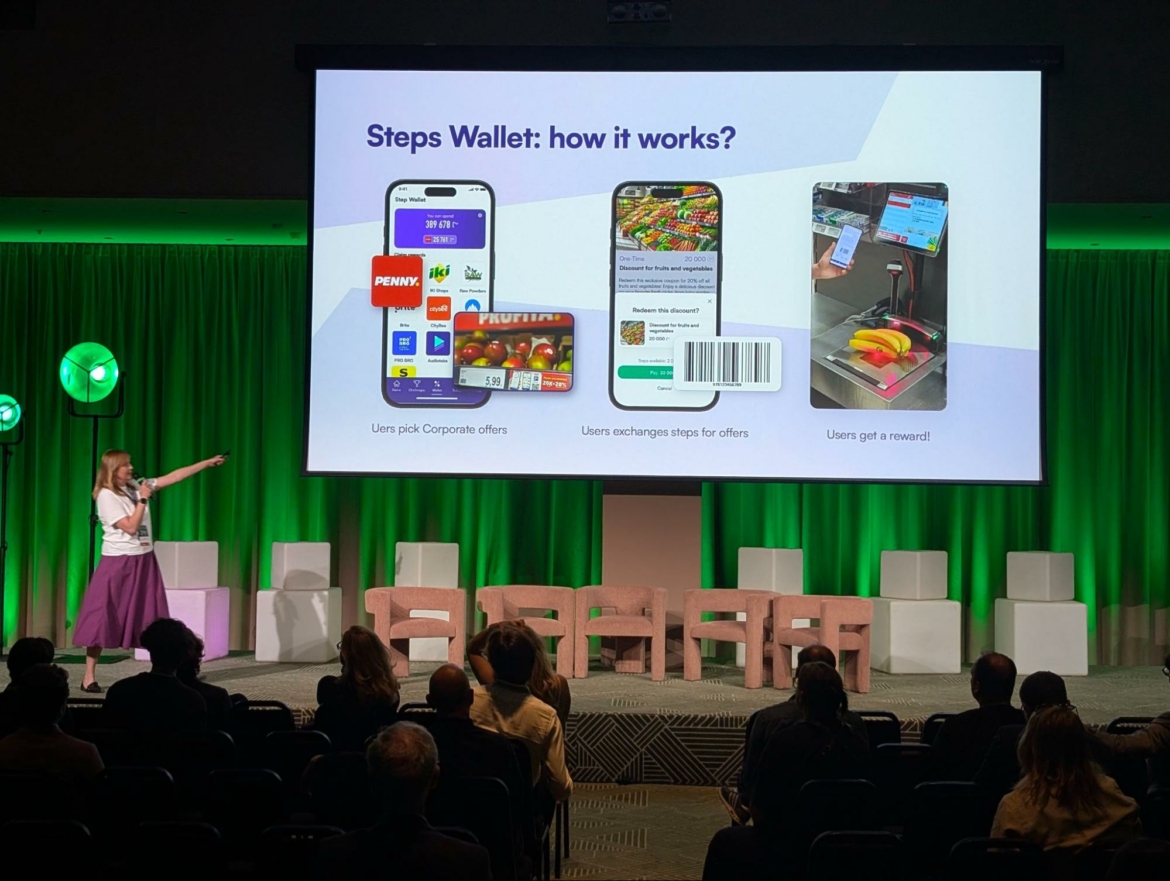

Some of the startups in this area included Blocksport, which focused on helping sports organizations turn fan engagement and first-party data into revenue campaigns, as well as Walk15, which showed how a walking app can become B2B infrastructure for employee, community, and sports engagement.

Vlada Musvydaitė pitching Walk15

The “coopetition” panel made the same point at an ecosystem level: sports innovation is not only about apps or fan engagement tools. It also depends on market access, city and university ecosystems, sports bodies, EU funding knowledge, and bridges into other regions.

"Embracing “Coopetition” for a Stronger Ecosystem", featuring Juan Fuentes (GSIC/EBAN Sports), Alberto Bichi (EPSI), Mike Yang (ABSG), Kamil Kazim Sari (Sport Singularity), Taija Lappeteläinen (City of Jyväskylä), Alina Adomaitytė (Lithuanian House of Basketball)

There were many more startups across these sectors, but I want to avoid turning this into a full pitch catalogue. The pattern is what matters: each domain creates its own risks for investors to test, from science and regulation to procurement, hardware scale-up, content rights, data reliability, engagement quality, and founder-market fit.

The value between sessions

At EBAN Vilnius, the informal layer was not separate from the investment layer. It is often where people test whether a pitch, a founder, a technology, or a market story still makes sense after the formal session ends. It also gives investors and founders room to explore questions that did not fit into the formal sessions.

A break conversation I had with Laura Anne Edwards focused on the same founder-role question from the sessions: what if the person who built the company should not be the long-term CEO?

The useful answer is not necessarily a choice between staying and leaving. Instead, it’s about designing the role around the founder’s strengths, life and/or company stage, and willingness to build, scale, delegate, or bring in leadership.

In another informal chat around space and defense, Franziska Bäurle shared a “777” fast iteration cycle approach that was a useful counterexample to the idea that deeptech and defense innovation must always move slowly.

The practical lesson was about scope: identify a capability gap, find existing startup-ecosystem technology that might fit, build a narrow MVP, and scale only after the problem has been made small enough to test.

Practical takeaways

Across the sessions, pitches, and informal conversations, the practical takeaway was less about any single sector and more about what each audience should test earlier.

For founders: strong technology needs timing, team clarity, customer feedback, and disciplined investor follow-up.

For angels: sector expertise matters more when companies are deeptech-heavy and harder to evaluate through generic startup metrics.

For universities and venture builders: spin-offs are easier to fund when founder roles, IP, customer discovery, and early funding choices are handled before they become problems.

For cross-border investors: a startup may work well in one country, but scaling across borders still depends on local partners, customer proof, and knowledge of how that market works.

Closing

The most useful part of EBAN Vilnius was not only seeing which startups pitched well. It was seeing how founders, angels, universities, venture builders, and ecosystem builders were trying to translate technical depth into investable, usable companies.

That kind of work rarely fits into one panel or one pitch. It was visible in the formal sessions, in the sector-specific startup batches, and in the conversations between stages.

Thank you to EBAN, LitBAN, and everyone who made the event possible. I’m looking forward to the follow-up conversations and to the next opportunity to attend.

Jacopo Losso (EBAN) and myself, Mihai Aperghis (TechAngels)

About the author

Mihai Aperghis is an entrepreneur and angel investor with TechAngels Romania, an EBAN member network. He is the founder of vertify.agency, an organic growth agency, and Search Analytics for Sheets, a SaaS product for search analytics. His work combines product development, growth strategies and early-stage technology investing.

Welcome to the EBAN Members Section! Login to get access to dealflow, discounts on international events, access to dedicated learnings and more.

Register using the code given by the EBAN member organisation you are affiliated to.